A FICO credit score is a number ranging from 300 to 850 (up to 900 for certain industry scores) that’s calculated using information from your credit reports.The Fair Isaac Corporation (FICO) introduced the first FICO credit bureau risk score in 1981. Since then, the FICO score is now recognized as a highly reliable source for credit information.

Your FICO score is important because many creditors use it to inform their decisions about their relationship with you. For example, a high FICO credit score increases your likelihood of getting approved for loans and credit cards. On the other hand, a low score is likely to hike up your interest rates.

Knowing your FICO score is also helpful when fixing your credit and preparing for large purchases like a new home. To get you started, we’ve broken down everything you need to know about your FICO credit score in our guide below.

What Is the Difference Between Your FICO Score and Your Credit Score?

Your FICO credit score is the score determined using FICO’s scoring model while your credit score refers to the number calculated by any scoring model (such as VantageScore). VantageScore uses their own scoring criteria with features like clear “reason codes” why scores aren’t higher. To make matters even more confusing, you also have multiple FICO scores. Below, we explain why this is and what you need to know about your different scores.

Why Are There Different FICO Credit Scores?

There are different FICO scores because lenders use different types of scores the bureaus use different data to report FICO scores.

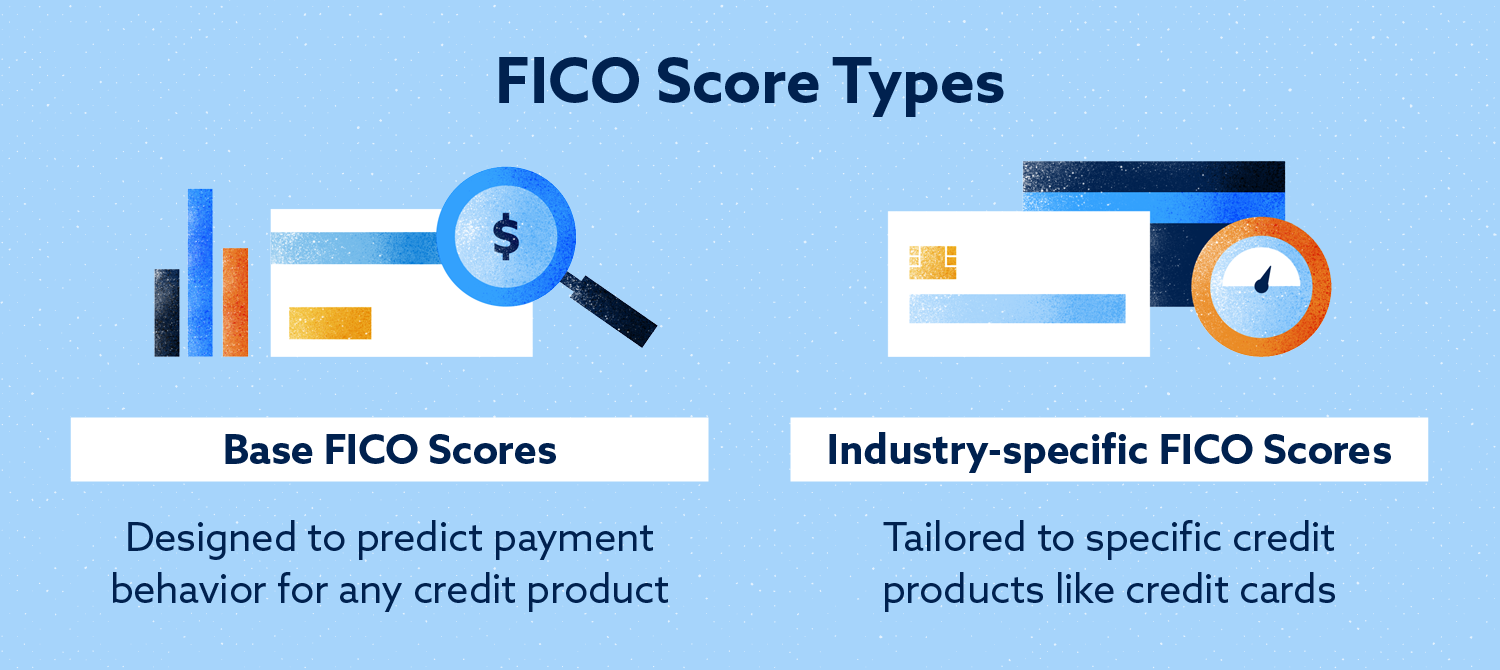

First off, there are two types of FICO scores: base scores and industry-specific scores.

- Base FICO scores: This is the most commonly used type of score designed to predict late or missed payments for any credit product.

- Industry-specific FICO scores: This score is tailored to specific credit products like mortgages and credit cards. FICO Auto Scores and FICO Bankcard Scores are two examples of industry-specific scores.

In addition, there are multiple FICO score versions. FICO has updated its score model over the years to accurately reflect changes in society like our use of credit and evolving requirements from lenders. FICO’s most recent version is FICO Score 9, but FICO Score 8 is still widely used.

Finally, scores can differ based on the reporting credit bureau. Scores can differ slightly since:

- Your credit information varies with each credit bureau. Some lenders report to all three bureaus while others do not. This results in inconsistent scores across the bureaus.

- Lenders can decide if and when they upgrade to the newest FICO scoring model. This means lenders are free to use FICO Score 8 or older models even if newer models are released.

You can ask your creditors what type of score and version they’re using so you can understand the criteria you’re being evaluated against.

What Is a Good FICO Credit Score?

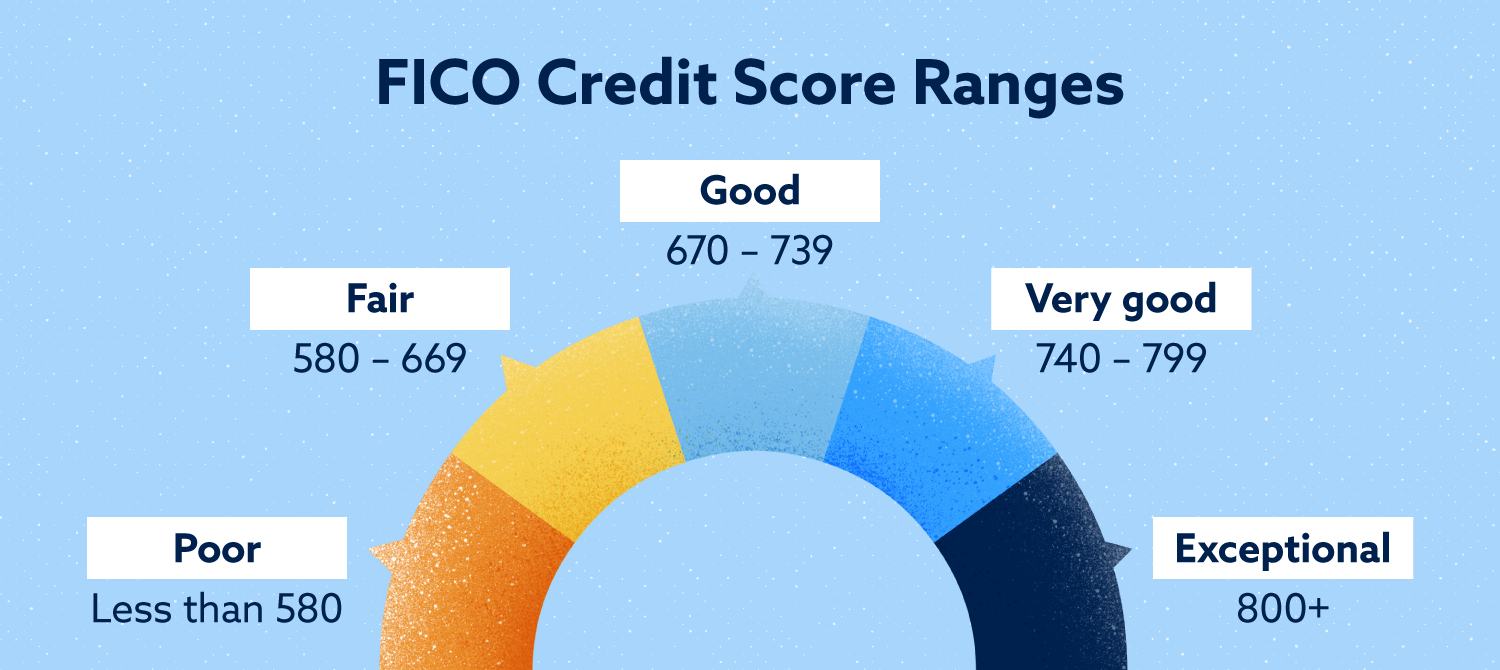

A FICO score in the “good” range is a score that falls between 670 and 739.

However, you can achieve a higher score since the FICO credit score can go as high as 900. Take a look at the list below to see what rating each score range falls under and what constitutes a good credit score.

- Less than 580: Poor

- 580 to 669: Fair

- 670 to 739: Good

- 740 to 799: Very good

- 800+: Exceptional

Keep in mind that lenders have their own criteria and guidelines they use to make lending decisions. Many use other factors, like monthly income, in addition to your credit score to decide if you meet their requirements.

What Factors Affect Your FICO Score?

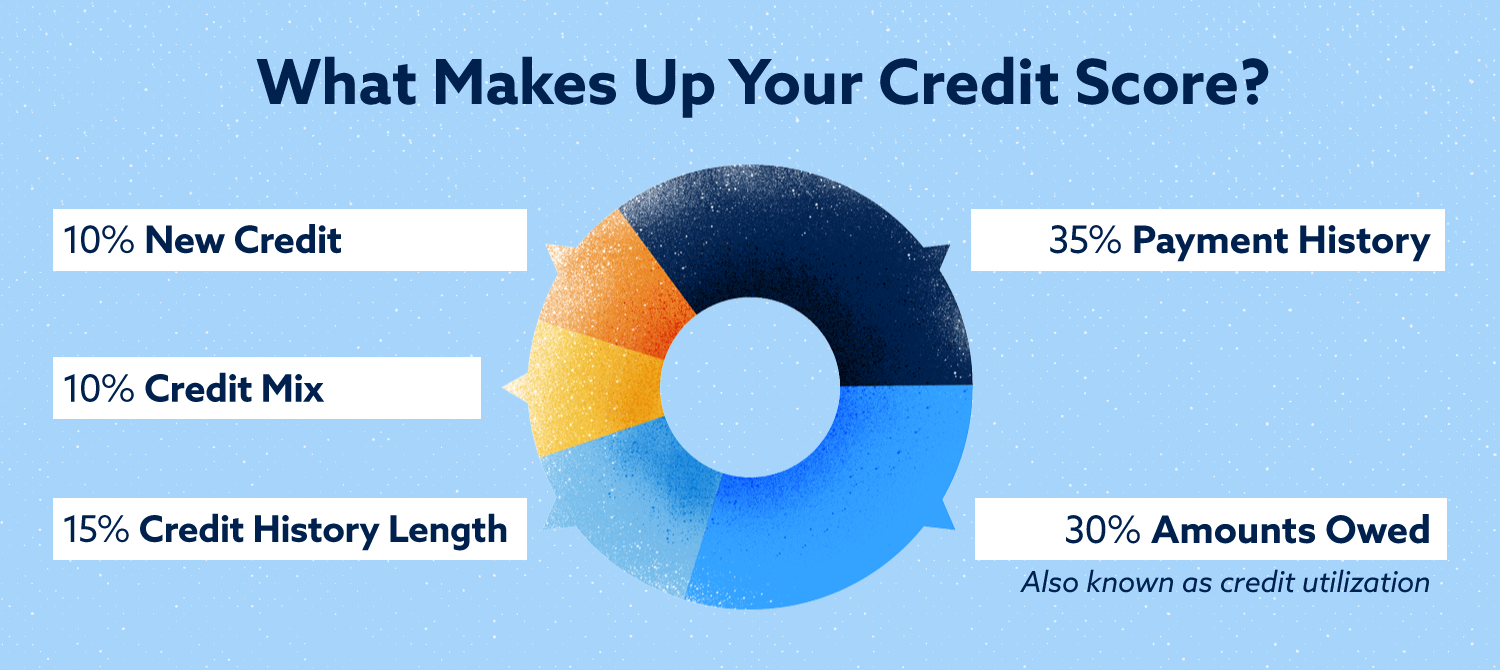

FICO credit scores are determined by five categories: payment history, amounts owed, credit history, mix of credit and new credit. Actions that fall under these categories can raise or lower your score. For example, opening too many credit card accounts at once can lower your score.

You can learn more about the all five FICO score factors below.

- 35 percent – Payment history. The biggest impact on your score comes from your ability to consistently make payments on time. Late and missed payments hurt your score.

- 30 percent – Amounts owed. The amount of money you owe compared to the amount of credit you have available makes the second largest impact on your score. This ratio is also known as your credit utilization. The lower your credit utilization, the better your score.

- 15 percent – Length of credit history. The next most impactful category is your credit age. Longer credit histories give credit bureaus a bigger picture of your past payments and other behavior.

- 10 percent – Credit mix. The types of credit you have also make a small impact on your credit score. Successfully managing a mix of credit cards, mortgage loans and other things can give your score a positive bump.

- 10 percent – New credit. Opening multiple credit accounts in a short period of time can make a small, negative impact on your score.

Attempting to open accounts results in multiple requests, known as hard inquiries, that also negatively impact your score. Multiple hard inquiries and new accounts in a short period appears risky to lenders, especially for people who have short credit histories.

There are several ways you can check your credit score and credit report to see where you stand and what information each bureau has on you. Learning how to evaluate your credit report is important to ensure your information is reported accurately and fairly.

How Do You Keep Your FICO Credit Score Accurate?

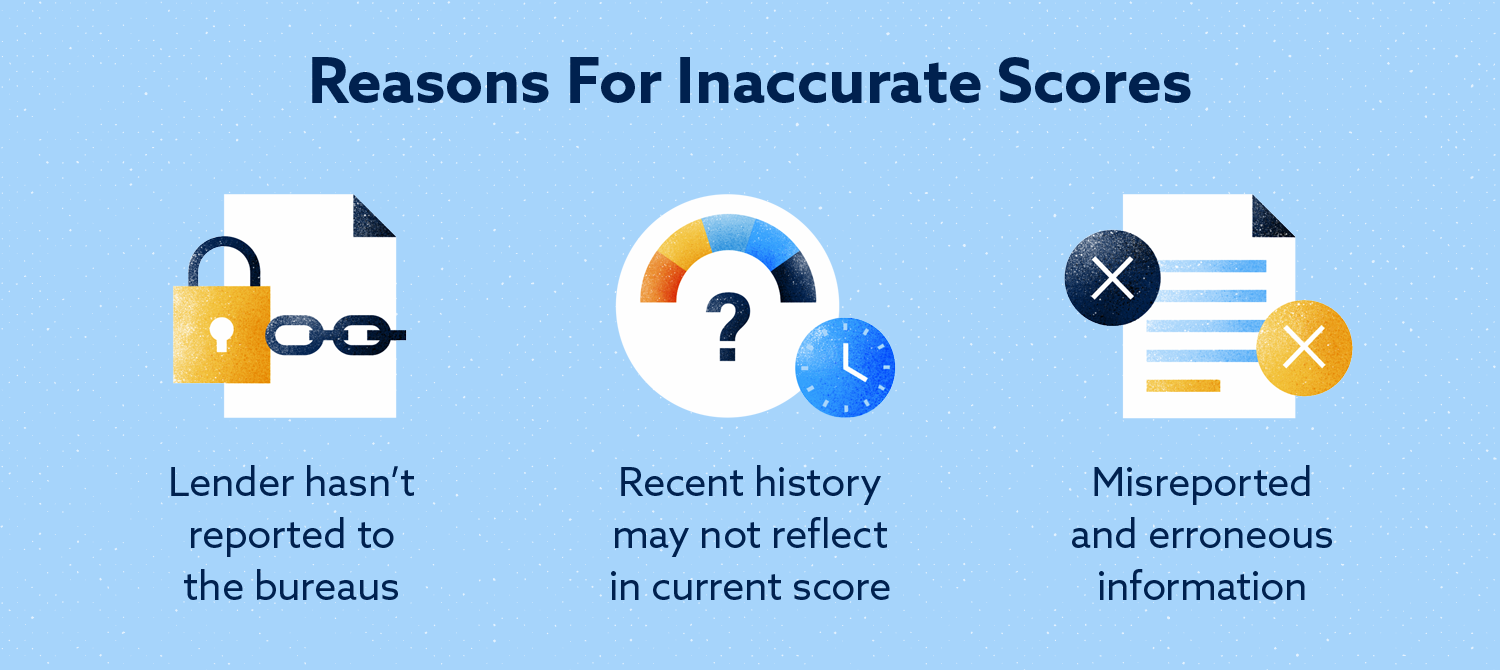

While you’re actively working on building your credit and improving your FICO score, you may notice that your scores don’t seem to reflect all of your hard work.

This is due to a number of things. Your lender might not have reported to the bureaus, your recent history might not be reflected in your current score, or you could have an error (or errors) on your credit report. It’s crucial to periodically check your score and report since some errors can drastically and unfairly drop your score.

Mckenzieadams.net provides and monitors your FICO credit score as a part of our suite of paid services. In addition to credit monitoring, we also contact the bureaus on your behalf to ensure your information is accurate and up to date. Learn more about our credit repair services to see how we can help you fix your credit and ensure your information is fairly reported.

***Call us NOW at (888) 810-2897 or visit mckenzieadams.net to learn how to Protect and Improve your credit RIGHT AWAY***