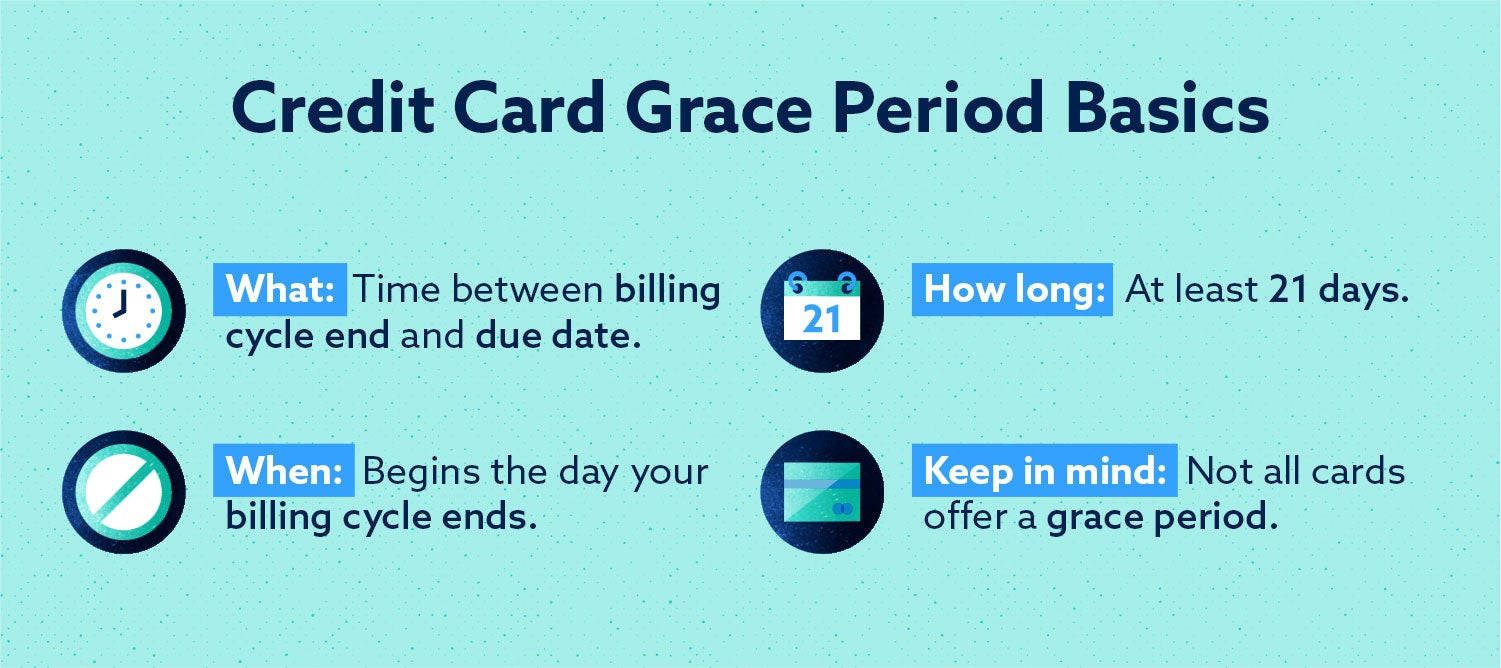

A credit card grace period is the time between the end of your billing cycle and your payment’s due date that allows you to pay your balance without incurring interest or penalties.

Missing a credit card payment is never a good idea. It can not only hurt your finances by adding late fees and increasing the interest on the balance you owe, but it can also lower your credit score. Luckily, most credit cards give you a grace period.

For that reason, a credit card grace period is always good to have, but it’s also important to understand. The grace period gives you an extra amount of time to pay your credit card bill before your credit card issuer considers it late and applies late fees or penalty interest. However, your grace period benefits depend on the terms laid out by your credit card issuer.

Read below to learn how a grace period works and how it affects both your credit and your finances.

How Does a Grace Period Work?

Like we mentioned earlier, a grace period is the time your given to pay your bills without getting penalized. The grace period usually lasts between 21 and 25 days and starts the day the billing cycle ends. The end of the billing cycle is sometimes referred to as the statement date or the closing date.

Do All Credit Cards Have a Grace Period?

Most credit cards offer a grace period. However, credit card issuers are not required to provide one, and if they do, there are certain legal guidelines they must follow. Your card agreement will tell you if you have a grace period and for what length it is. You can also sometimes find this information on your monthly statement.

Some transactions don’t have a grace period. Convenience checks and cash advances generally incur interest from the date of the transaction, even if you have no outstanding balance on the card.

If your credit card offers a grace period, it’s important to understand your rights and the parameters your credit card company must follow.

CARD Act of 2009

The Federal Credit Card Accountability, Responsibility and Disclosure Act of 2009 (also known as the CARD Act) requires credit card companies to give cardholders at least 21 days to pay their bill before it’s considered late. This means you must receive your bill 21 days prior to your due date. It also requires grace periods to be at least 21 days. You can still accrue interest during this time period if your card does not have a grace period, however.

What Happens When You Pay Late?

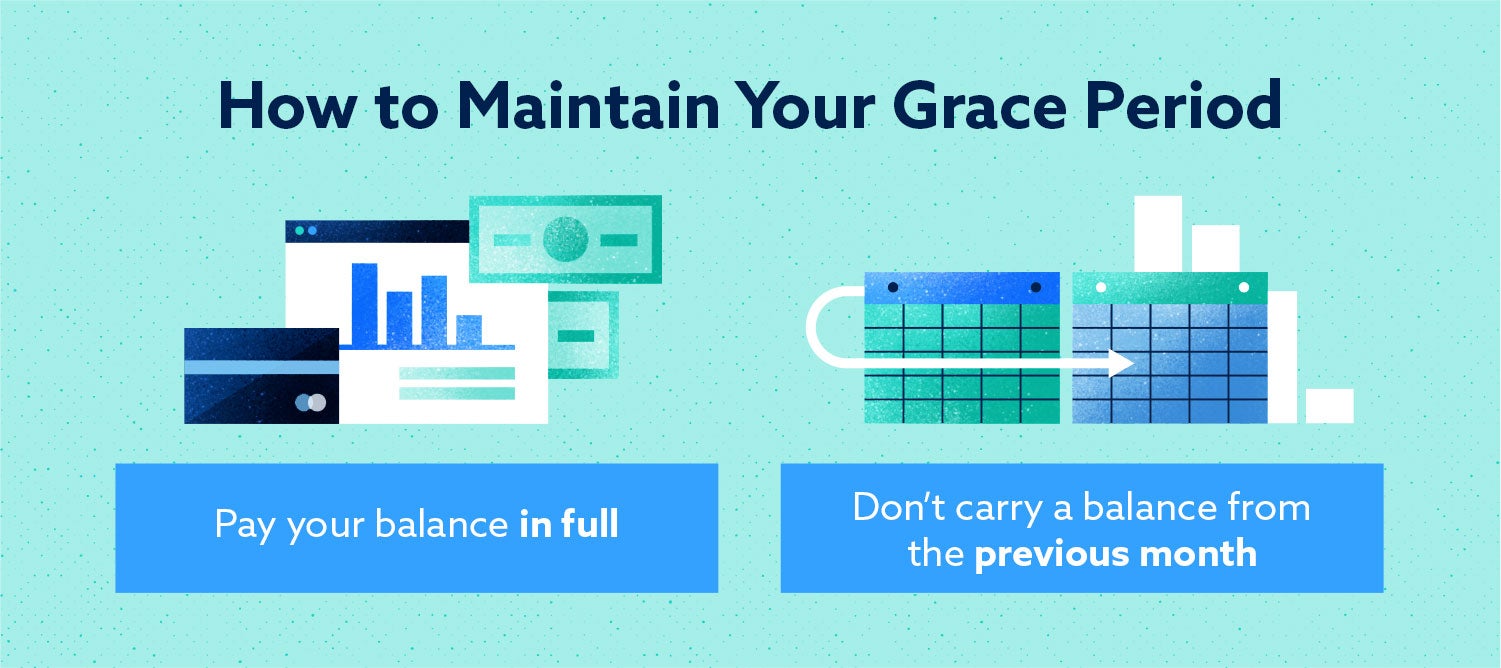

When you miss a payment, pay late or don’t make your full minimum payment, you may lose your grace period. Don’t worry—you can earn it back, but you may experience a lag between when you pay off your card and when the grace period kicks back in. You may have to pay off your charges for two consecutive months or longer before you regain your grace period.

Giving Yourself More Time to Pay

You can use your credit card’s grace period to give yourself more time to pay by understanding the terms of your card’s grace period, communicating with your lender and timing your purchases.

Change Your Billing Cycle

One thing you can do to give yourself more time is to ask your lender to change your billing cycle date. Doing so can help align your paycheck with your due date and potentially give you more time to pay your bill. Keep in mind that changing the due date might not apply to your current cycle, so you’ll want to confirm with your credit card company.

Time Your Purchases

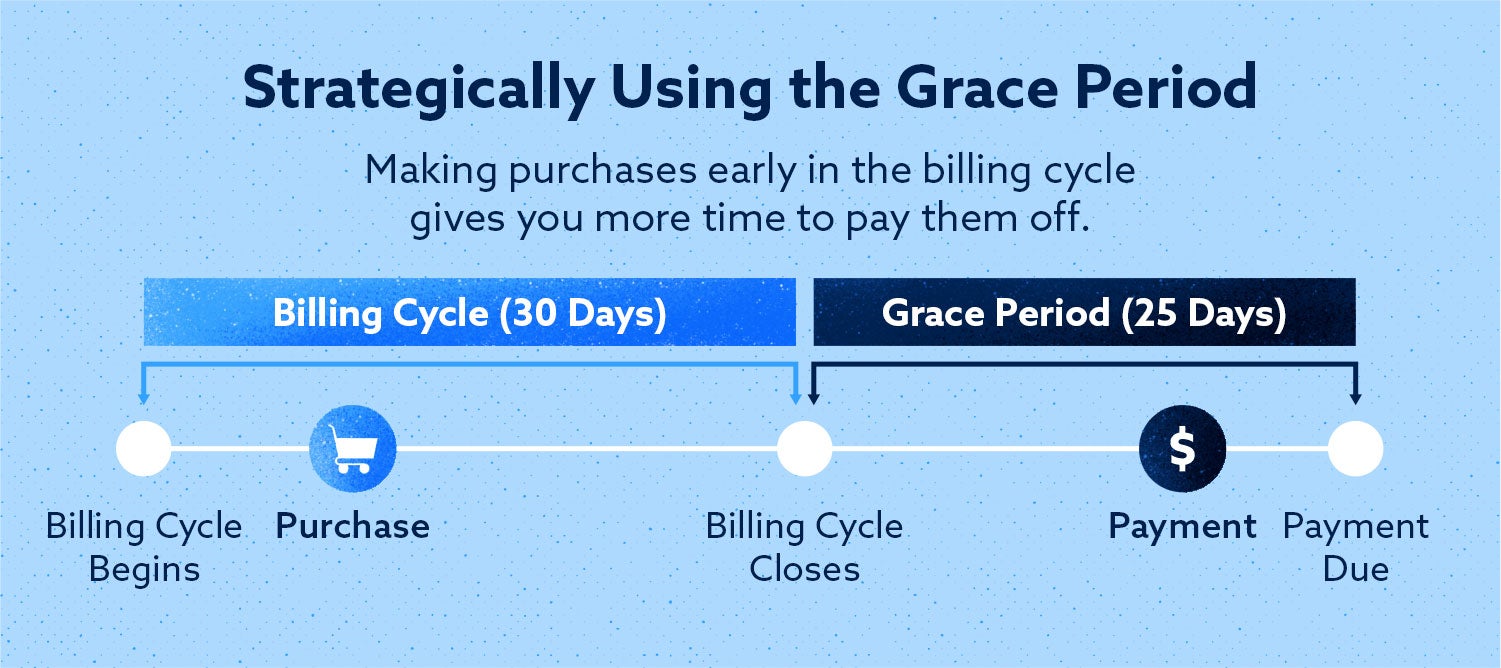

Another strategy is to make purchases immediately after your statement closing date. Doing this puts that transaction on the following month’s bill. You also have the benefit of that month’s grace period. This potentially gives you about a month to pay off the balance interest-free.

For example, let’s say you use your credit card to make a big purchase. Your statement closing date is March 3, so you plan to make a big purchase of $800 on March 4. This purchase will then appear on next month’s bill delivered on April 3 with a grace period ending on April 28. In this case, timing your purchase one day after your closing date can buy you extra time for saving extra money to pay off the purchase by the actual payment due date.

Things to Consider When Attempting to Prolong Your Grace Period

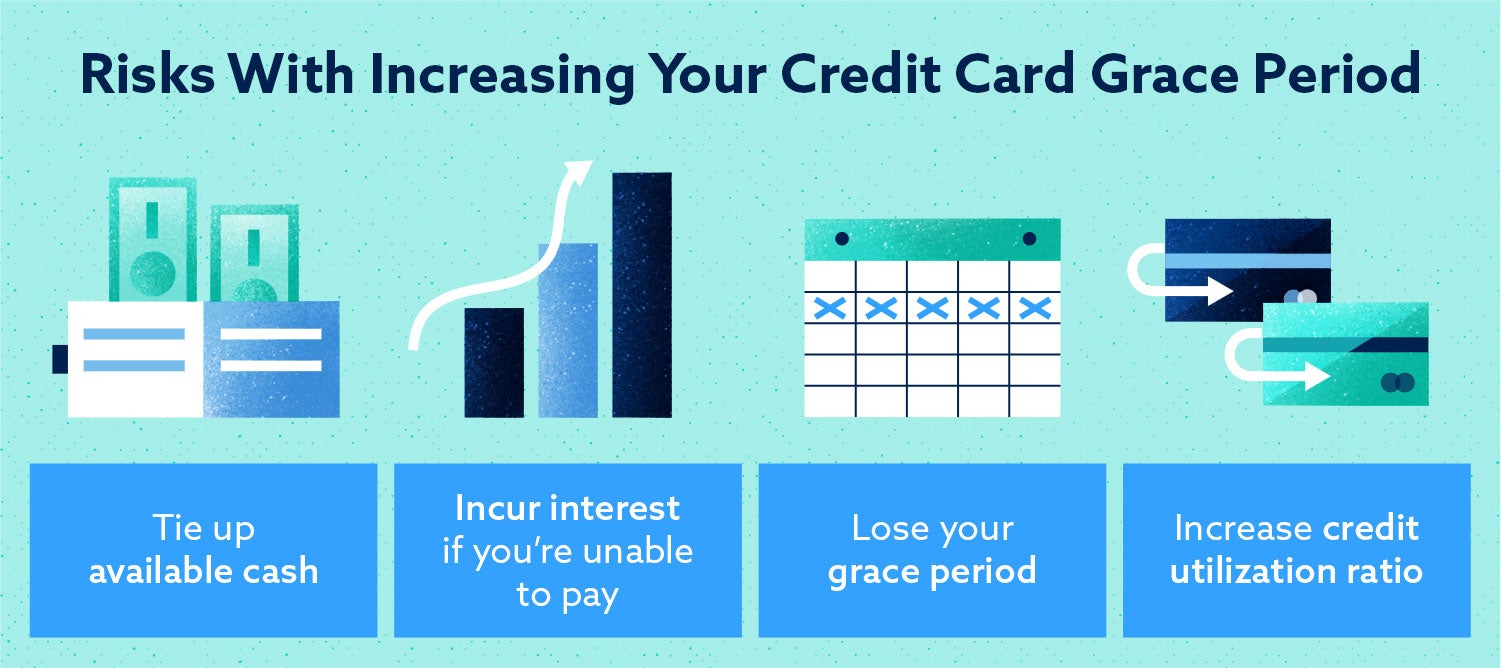

You should proceed with caution when attempting to prolong your grace period. Here are a few things that you should look out for when taking advantage of the grace period.

- Tie Up Available Cash: Payments towards paying down a large purchase takes away available cash from other things like groceries, gas and any unexpected expenses.

- Incur Interest and Lose Your Grace Period If You’re Unable to Pay: If you’re unable to pay down the large purchase before your grace period ends, you’ll incur interest and lose your grace period until you can pay it off.

- Increase Credit Utilization Ratio: Your credit utilization ratio is the comparison between the amount of credit you have available and the amount of credit you use. A higher ratio negatively affects your credit ratio until you’ve lowered it. Large purchases can also affect your credit utilization ratio.

Making a purchase you know you can’t pay off can quickly dig you into a financial hole and use your available funds. An emergency fund is important to have just in case your finances go south or an emergency arises while you’re paying down your balance. Above all else, you should still strive to pay off your balances as soon as possible.

How Credit Card Payments Affect Credit Score

Paying your bills on time and keeping low balances are just two ways to keep your finances and credit in check. If you’ve lost your grace period and are having trouble paying down multiple debts, we recommend you talk to a financial adviser to give you personalized debt solutions. If any late payments on your credit report are inaccurate or unfair, credit repair may be the answer. Our credit repair services can help resolve mistakes like these on your credit report.

***Call us NOW at (888) 810-2897 or visit mckenzieadams.net to learn how to Protect and Improve your credit RIGHT AWAY***