A secured credit card is one in which you make a cash deposit. The credit card issuer keeps that deposit as collateral in case you don’t pay what you owe on the card. Secured cards are helpful for people who have no credit history, thin credit history or bad credit. Secured cards can also be ideal for people who would like to test out the idea of credit cards while having protection in place so they don’t rack up a lot of debt. In general, though, people turn to secured cards when they do not qualify for unsecured cards. Secured cards can be a way for you to build or rebuild your credit score. With that in mind, here’s the answer to the question, “How does a secured credit card affect credit score?”

The Interplay Between Your Credit and a Secured Card

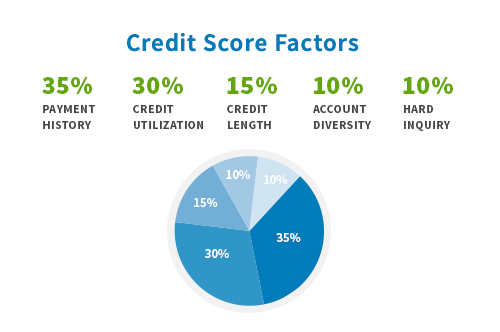

Remember, not all secured credit card issuers report your good behavior to all the credit bureaus. When you’re comparing secured cards, look for issuers that report to all three credit bureaus. The following impact your credit score:

- Credit mix (10%)

- Inquiries (10%)

- Length of credit history (15%)

- Utilization ratio (30%)

- Payment history (35%)

First, your credit mix shows you’re capable of handling various types of credit accounts such as a card, car loan and student loan. You should be able to add a secured card when there was no credit card before to make your profile look better.

Next, inquiries occur when a lender or credit card company checks your profile before deciding whether to give you credit. You may be applying for an unsecured card but get offered a secured card, or you could be applying for a secured card in the first place. A hard inquiry is likely to decrease your credit score slightly for about a year. One application for a card should be fine. Two should be as well. More than that and the points can add up to seriously ding your score. Hard inquiries remain on your credit history for about two years.

Length of credit history is the age of each credit account you have. Ideally, your history would show accounts that you’ve maintained for a long time. Usually having credit for a long time can help your score.

Utilization ratio is the level of debt you tend to carry relative to your credit limit. If your secured card is the only credit you have and you don’t charge much on it, your utilization ratio will be low, which is good. On the other hand, if you often max out your card, your ratio will be high, which isn’t so good. The lower your ratio, the more it helps your score. Secured cards often don’t have high limits, so it can be difficult to keep their utilization ratio low. One way to deal with this is to pay your bill a few times over the statement period.

Last but not least is payment history. It’s the most significant individual driving force in your score. Making payments in full and on time will help your credit score.

If you’re wondering whether having an unsecured card compared with a secured card affects your score, it does not. A card may not even show up as secured on your history. That depends on how the issuer reports it. Where the difference may come into play is with lenders who want to see your capability to handle unsecured credit.

If your ultimate goal with a secured card is to use it to improve your credit score or to get a large loan such as a mortgage, focus the most on paying balances in full every month, making timely payments and keeping your charges low compared to your limit. That’s how a secured credit card can affect your credit score in a great way.

How High Can the Limit Get on a Secured Card?

The limits on secured cards typically aren’t very high, but it’s possible to find some that go to $10,000. On the other end of the spectrum, the minimum is usually $200. Whatever the limit is, that is normally the amount of money you deposit as the issuer’s collateral. So, you’d put down $500 for a card with a limit of $500. Check each card issuer to see if it lets you make a larger deposit for a higher limit.

Responsible Use of a Secured Card

Like with regular credit cards, many secured cards charge fees (service, monthly, annual and so on). However, it’s fairly easy to get a secured card that doesn’t charge fees. Doing your research and finding a card that doesn’t charge these types of fees can save you money in the long run.

You do have to consider interest rates unless you’re sure you’ll pay your balance in full each month. Interest charges add up and can make it more difficult to pay off your card balance when you’d like to transition to an unsecured card.

In any case, it’s well worth your while to research interest rates and fees. You can get fee-free secured cards from the issuers below:

- Navy Federal Credit Union

- Discover®

- State Department Federal Credit Union

- Capital One®

- Bank® / Harley Davidson®

- DCU®

Check out each issuer’s website to see if you qualify for a card.

Quick Facts About Secured Cards for Long-Term Credit Score Planning

It’s good to take both a short-term and long-term approach to your credit score. When you get a secured card, keep a few things in mind for the big picture.

Perhaps most important is that some credit card issuers upgrade secured card to an unsecured card after six months to a year of responsible use. Some credit card companies do this automatically, so keep an eye on that if you prefer to keep using a secured card. You get your deposit money back when your card transitions from secured to unsecured or if you close your secured account with a fully paid-off balance.

A secured card can sometimes be confused for a prepaid card. With a prepaid card, the amount you paid at first is subtracted from the card balance with each item purchase you make until the balance reaches zero. With a secured card, you make payments like you would with a regular credit card. If you pay less than the full balance each month, interest charges apply.

A Secured Card Can Help Your Credit Score Just as Much as an Unsecured Card

Many people wonder, “How does a secured credit card affect credit score?” Put simply, a secured card can help your credit score just as much as an unsecured card. That’s why you can use secured cards to establish a good payment history, keep your utilization ratio low and begin a credit file. You will not get a lower credit score for merely having a secured card. Just keep in mind that lenders want to see you’re capable of handling all types of credit.

Has Your Credit Score Been Affected?

If your credit score has decreased, you can begin fixing your credit today. Find out here how to start. Also, like us on Facebook and follow us on Twitter for more information.

Article Updated July 1, 2019

***Call us NOW at (888) 810-2897 or visit mckenzieadams.net to learn how to Protect and Improve your credit RIGHT AWAY***